Hydrogen Transportation After HVS: Narrow Niches, Big Subsidies, Long Pilots

Infographic of hydrogen transportation commercialization assessment by author with ChatGPT

May 12, 202631 minutes

Michael Barnard

0 Comments

Support CleanTechnica's work through a Substack subscription or on Stripe.

Infographic of hydrogen transportation commercialization assessment by author with ChatGPT

May 12, 202631 minutes

Michael Barnard

0 Comments

Support CleanTechnica's work through a Substack subscription or on Stripe.

HVS was not a fringe hydrogen truck company with a sketch and a slogan. It had a serious ambition, a real engineering team, public support, private funding, partnerships, prototypes, and a target market that sounded plausible enough: zero-emission heavy-duty freight. Hydrogen Vehicle Systems wanted to build fuel-cell trucks for a world in which diesel had to leave road freight and batteries were still being framed as too heavy, too slow to charge, or too limited for long-haul duty cycles.

HVS appears to have raised or attracted at least £55 million in private and public backing, including £30 million from EG Group and about £25 million in UK government support, before entering administration and seeing its remaining assets and intellectual property sold for £145,000 recently. That number is the useful part. It compresses years of hydrogen trucking ambition into something much closer to salvage value than venture value. It does not mean the engineers did poor work. It does not mean the problem was imaginary. It means the business case did not close around the engineering. A truck company is not a truck. It is a truck, a factory, a supply chain, customers, service operations, fuel supply, refueling infrastructure, warranties, financing, and enough volume to make all of that more than a demonstration.

That was the trigger for me to go back to my hydrogen transportation dataset. HVS was the sharp event, but the better question was whether it was an outlier. Hydrogen transportation has produced a long stream of announcements across trucks, buses, trains, cars, aircraft, ships, ferries, tractors, excavators, taxis, refueling stations, fuel-cell systems, and hydrogen production for mobility. Some of those initiatives are still active. Some are in service. Some are gone. Many are somewhere in the fog between a press release and a market.

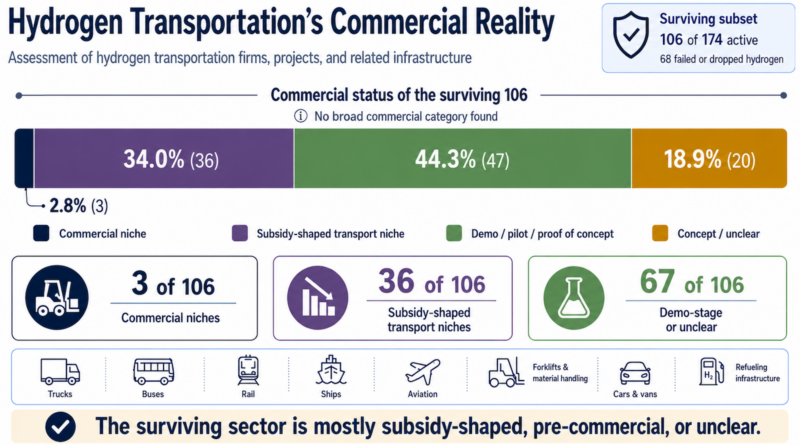

The dataset now contains 174 firms and projects that promoted hydrogen for transportation or related mobility infrastructure. That does not mean every one was a pure vehicle company. Some were fuel-cell suppliers, some were refueling firms, some were industrial hydrogen incumbents, some were aviation startups, some were bus manufacturers, and some were project vehicles around ammonia, e-fuels, or hydrogen corridors. The common thread was not corporate structure. It was the claim that hydrogen had a transportation role.

Of those 174 entries, 68 had failed, dissolved, or dropped hydrogen. That is 39.1% of the total. The remaining 106 were still active, or at least still presenting some hydrogen transportation relevance. They sorted into four categories: commercial niches, subsidy-shaped transport niches, demo, pilot, or proof-of-concept activity, and concept or unclear status.

I used “commercial niche” in a narrow way. It does not mean a company is commercially successful somewhere else while also talking about hydrogen mobility. It means the hydrogen transportation use case itself has repeat customers, operating assets, and a plausible operating logic that is not mainly subsidy-dependent. On that basis, the surviving dataset has only 3 commercial niches out of 106, or 2.8%. Those three are all in material handling: Plug Power’s GenDrive systems, Raymond or Toyota hydrogen-compatible material handling, and Toyota Material Handling fuel-cell forklifts. The hydrogen warehouse is more real than the hydrogen highway. Note that Plug Power is part of the group of hydrogen companies with Ballard Power and FuelCell Energy whose real business strategy appears to be surviving between hype-driven capital raises, bleeding capital until the next one and diluting the equity of successive rounds of investors.

I used “subsidy-shaped transport niche” for vehicles, stations, or deployments where the market is strongly shaped by public procurement, grants, mandates, national industrial policy, hydrogen corridors, or refueling support. That category contains 36 entries, or 34.0% of the surviving set. It includes hydrogen buses, passenger cars, taxis, rail projects, truck fleets, refueling networks, and Chinese policy-cluster vehicle deployments. These are often machines in service. But their economics and procurement conditions are not normal market adoption.

The largest category is demo, pilot, or proof of concept. It contains 47 entries, or 44.3% of the surviving set. This is where a large share of hydrogen transportation still lives: field trials, prototype fleets, certification programs, route tests, hydrogen excavators, aircraft demonstrators, train pilots, truck corridors, ammonia vessel concepts, and refueling trials. Demonstrations are useful when they reduce uncertainty. They become a market signal when the same sectors remain in demonstration mode for decades.

The final category, concept or unclear, contains 20 entries, or 18.9% of the surviving set. These are firms or projects that still have some public hydrogen transportation narrative, but current evidence of active deployment, product sales, or material progress is weak, stale, ambiguous, or hard to verify. This category matters because hydrogen projects often do not die with a clean obituary. They fade, pause, rebrand, wait for funding, move into “next generation” planning, or sit on websites as if time stopped at the last grant announcement.

Taken together, 67 of the 106 survivors are demo-stage or unclear, and another 36 are subsidy-shaped. That leaves 3 narrow commercial niches and no broad commercial category. The dataset does not say hydrogen transportation has disappeared. It says it has been contained.

The HVS failure makes more sense in that context. Hydrogen trucking is one of the hardest places to build a business because the truck is only the visible part of the system. The vehicle is expensive. The fuel is expensive. The refueling station is expensive. Maintenance is more specialized. The truck fleet needs high utilization to justify the refueling station, while the station needs high utilization to bring down delivered fuel cost. The hydrogen supply chain must be built before the vehicle market exists, yet the vehicle market needs the fuel supply chain before customers will buy at scale. That is a nasty sequencing problem.

Battery-electric trucks are not simple either. Depots need chargers, transformers, interconnection studies, sometimes battery storage, route planning, driver training, and operational discipline. But they plug into the electricity system, and their core components ride global battery, motor, inverter, and power electronics learning curves. HVS had to raise money not just for a truck, but for a network logic that had to mature around the truck. That is why the £145,000 sale matters. It is an ecosystem-financing failure as much as a startup failure.

Looking across the sectors shows why the category counts matter. The same pattern appears in different forms: a controlled setting, a public buyer, a grant-funded corridor, an incumbent keeping options open, or a demonstration program standing in for a market. Hydrogen transportation is not one sector. It is a collection of claims, and the evidence has to be tested claim by claim.

Material handling is the exception that proves the rule. Hydrogen forklifts can make sense in very large warehouses and distribution centers because the site is controlled, refueling is centralized, equipment can run multiple shifts, downtime is measurable, and safety and maintenance are professionalized. The geography is tiny, which matters because the hydrogen fuel system does not have to spread across a city, highway network, or continent.

This is also a legacy niche. Hydrogen forklifts gained a foothold when lead-acid battery fleets were more operationally awkward, with battery rooms, swaps, watering, and longer charging routines. Modern lithium-ion forklifts have eroded all of that advantage through opportunity charging, lower maintenance, and simpler integration with the electricity system, and are selling 30 times as many units every year as the total deployed hydrogen forklift fleet. In that narrow setting, existing sites continue because the infrastructure and supplier relationships are already in place.

But that is not a general transportation story. It is a bounded industrial logistics story. The conditions that make a hydrogen forklift case work are almost the opposite of the conditions in passenger cars, taxis, long-haul freight, aircraft, and ships. The warehouse contains hydrogen’s disadvantages. The open transport system exposes them.

Hydrogen buses deserve careful treatment because they are the most visible counterexample. Hyundai, Solaris, New Flyer, Wrightbus, CaetanoBus, Toyota’s bus work, Yutong, Foton, Feichi, Golden Dragon, Higer, and Zhongtong all have hydrogen bus activity. Some have deployments. Some have repeat orders. South Korea has put thousands of fuel-cell buses into service. European transit agencies have bought Solaris and Wrightbus hydrogen buses. North American agencies have ordered New Flyer fuel-cell buses. These are not imaginary vehicles.

But calling them broadly commercial confuses vehicle existence with market viability. Hydrogen buses are bought by public agencies inside policy frameworks. The bus purchase always receives support. The refueling station always receives support. The fuel supply chain often receives support. The procurement is tied to zero-emission mandates, hydrogen strategies, local industrial policy, or demonstration funding. CaetanoBus and the Toyota H2.City Gold are useful examples. The buses are on roads, but the company’s financial condition and the structure of hydrogen bus procurement do not support a conclusion that this is a robust unsubsidized commercial market.

The clean distinction is that battery-electric buses are often subsidy-accelerated, while hydrogen buses remain subsidy-dependent. Battery-electric buses receive public money too. They need depot upgrades, chargers, grid connections, route planning, and sometimes operational redesign. That is not in dispute. The question is whether the subsidy accelerates a technology that is already riding broad cost curves, or whether it holds up an ecosystem that otherwise does not clear the market. Battery-electric transit plugs into the electricity system and the same battery industrial base that supports cars, vans, trucks, stationary storage, consumer electronics, grid flexibility, and power tools. Hydrogen transit needs the bus, the fuel-cell system, the tanks, the station, the hydrogen production or delivery chain, and the maintenance regime to mature together. One is an extension of a huge electrification ecosystem. The other is a specialized fuel ecosystem built around small fleets.

And as I noted recently, new hydrogen bus orders have declined substantially in 2024 and 2025 in both Europe and North America, with 2025’s new deliveries being a lagging indicator of years old enthusiasm. Meanwhile, 70,000 battery electric buses were sold in 2024.

Passenger hydrogen cars are evidence of market weakness, not commercialization. Toyota Mirai, Hyundai Nexo, and Honda’s CR-V e:FCEV are technically available in some places, but availability is not broad commercialization. Volumes are tiny. Refueling geography is constrained. Fuel prices are high. Subsidies in South Korea are up to 60% of the sticker price of the cars, with more subsidies for the hydrogen. Station reliability has been a chronic problem in California, with only 7 stations having hydrogen recently. Resale values have been punished where fuel availability and pricing are poor. BMW’s iX5 Hydrogen remains a future low-volume option rather than a mass-market car. Hydrogen taxis, whether in Berlin, Saudi pilots, or the Uber and HysetCo Paris announcement, improve utilization compared with private cars, but they do not solve the fuel-system problem.

Stadler’s FLIRT H2 in California, Siemens’ Mireo Plus H orders, JR East’s HYBARI test train, Hyundai Rotem’s hydrogen train concepts, and CPKC’s hydrogen locomotives all show activity in rail. Hydrogen rail can make sense where routes are non-electrified, wires are politically difficult, and batteries are considered insufficient. But rail already has a dominant zero-emission solution: overhead electrification. Batteries cover some regional cases. Hydrogen rail mostly sits in edge cases, pilot fleets, public procurement, and specific corridors where other options are judged inconvenient. That’s why Alstom left the space entirely, although it was forced to buy Cummins rail fuel cell division in order to service the train sets that it had already sold.

Aviation contains some of the most ambitious hydrogen claims and some of the longest timelines. ZeroAvia, Beyond Aero, Stralis, Embraer and GKN, Fokker Next Gen, Project Fresson, Alaka’i, and Dream Fly all sit in the aviation part of the dataset. The technical work can be serious, but certification, volumetric energy density, storage, safety, range, payload, airport fueling, and aircraft redesign are large barriers. A hydrogen aircraft demonstrator is a technical achievement. It is not an airline market.

Maritime has a wider range of fuels and carriers, but the commercial pattern is similar. Sea Change in San Francisco, Kawasaki’s Suiso Frontier, Wilhelmsen’s Topeka, Hydrogenious LOHC, Hyrex before bankruptcy, Yara Clean Ammonia as a future shipping fuel, H2Carrier, Fuella, and Norsk e-Fuel all touch pieces of the maritime or fuel pathway. Ammonia, methanol, biofuels, and synthetic fuels may all play roles in shipping and aviation debates. But most hydrogen-derived marine fuel projects remain future-offtake, demonstration, or project-development stories. Moving molecules at sea is not the same as proving a current transport fuel market.

Construction and agriculture are full of plausible demonstrations and weak market pull. JCB’s hydrogen combustion program is real and technically active. Liebherr, Komatsu, Hyundai Construction Equipment, Volvo Construction Equipment, Kubota, AGCO/Fendt, and Applied Hydrogen have all explored hydrogen machines or retrofits. These sectors offer better control conditions than passenger cars because machines often work from depots, farms, mines, yards, or construction sites. But most evidence remains prototypes, field trials, engine approvals, and site tests. The procurement test has not been passed at scale.

Refueling infrastructure is its own trap. HTEC, TEAL Mobility, Everfuel, Atawey, Cavendish, ANGI, Air Liquide, Air Products, Chart, Hexagon Purus, Ryze, Vireon, John Cockerill, and others have station, storage, dispensing, or hydrogen infrastructure offerings. Some are functioning businesses. But a station supplier can sell into a grant-funded project while the vehicle market remains fragile. An industrial gas company can support mobility pilots while making money elsewhere. A refueling network can exist and still have low utilization, high delivered fuel cost, and too few vehicles to support expansion. Infrastructure activity is not the same thing as transport commercialization. I’ve done station utilization and profitability assessments in multiple countries and have yet to find one that looks like it’s paying for itself. There’s a reason that globally refueling stations are closing, not expanding.

China complicates the picture in useful ways. It has fuel-cell suppliers and vehicle firms, including SinoHytec, Sinosynergy, Refire, Toyota-SinoHytec, KENSINO, Farizon, Hybot, Yutong, Foton, Feichi, Golden Dragon, Higer, and Zhongtong. China’s hydrogen vehicle clusters put vehicles on roads and support domestic supply chains. That is material. But they are also policy-shaped by design. China is one of the best places in the world to make a hydrogen transport program visible and measurable, and also one of the best places to see how much larger the battery-electric alternative has become across cars, buses, trucks, vans, and charging. Approaching 100% of new bus orders in China are electric. 20% of heavy truck sales in 2025 were electric. It has thousands of electric garbage trucks on its roads. It has 700+ TEU battery electric container ships operating in coastal and river waters.

The persistence of pilots is not irrational. Hydrogen is technically real. Fuel cells work. Hydrogen combustion engines can run. Liquid hydrogen can be transported. Ammonia can carry hydrogen. Engineers can solve specific integration problems. Institutions like hydrogen because it offers industrial policy, energy security narratives, continuity for fuel suppliers, a role for gas infrastructure, and familiar refueling patterns. Pilots let companies and governments preserve options. The problem comes when option preservation is mistaken for market arrival.

HVS was the visible failure, but the dataset shows that visible failures are only one part of the story. From 174 assessed firms and projects, 68 have failed, dissolved, or dropped hydrogen. Of the 106 survivors, only 3 sit in durable commercial niches, all in material handling. Another 36 are subsidy-shaped, 47 remain demo or proof of concept, and 20 are concept or unclear. That is the quieter story HVS pushed back into view. Hydrogen transportation has not disappeared, but after decades of work its commercial territory remains narrow, supported, and heavily pre-commercial.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News! Advertisement Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here. Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent. CleanTechnica uses affiliate links. See our policy here.CleanTechnica's Comment Policy

Share this story!

Схожі новини

Chinese EVs & The US Market — Where Is This Going?

Genesis GV90 with coach doors found abandoned with no camouflage [Images]