High Stakes: How Much EV Investment Is At Risk Across Europe

May 12, 20261 hour

Transport & Environment (T&E)

0 Comments

Support CleanTechnica's work through a Substack subscription or on Stripe.

May 12, 20261 hour

Transport & Environment (T&E)

0 Comments

Support CleanTechnica's work through a Substack subscription or on Stripe.

A new study examines the ‘industrial opportunity cost’ of proposals to weaken EU car CO2 targets.

Spurred by the growing electric car market, much investment into EV production, batteries and components has been announced. But this is now at risk as the EU debates its car CO2 rules that will define the size of the market. This report looks into the industrial opportunity cost of various car CO2 proposals on the table.

From China to Chile, battery electric vehicles (BEVs) are now the growth engine of the global automotive industry, accounting for the vast majority of new investment, innovation and model launches. If Europe anchors BEV manufacturing — including batteries, power electronics, and critical components — within its borders, it can rebuild its industrial base, increase its domestic gross value added (GVA) and secure growth and jobs.

But the risk today is industrial decline through strategic hesitation. Despite much investment announced and affordable mass-market BEVs finally hitting showrooms, the EU is once again proposing to revise its 2030–2035 car CO2 rules (which define the size of the EV market). Compared to the current regulation, the new Commission proposal weakens both the 2030 and 2035 targets, while the auto industry wants to reduce that ambition even more.

This report estimates the industrial opportunity costs for BEV production, as well as battery and its value chain investment from these proposals. To do so, T&E uses three scenarios: the current CO2 regulation (REF), the Commission proposal (EU) and the auto industry position (LOW). Aside from the car emission rules, the industrial policy — notably the recently proposed Industrial Accelerator Act (IAA) is critical to ensure the EV market brings a local manufacturing base.

This report estimates the industrial opportunity costs for BEV production, as well as battery and its value chain investment from these proposals. To do so, T&E uses three scenarios: the current CO2 regulation (REF), the Commission proposal (EU) and the auto industry position (LOW). Aside from the car emission rules, the industrial policy — notably the recently proposed Industrial Accelerator Act (IAA) is critical to ensure the EV market brings a local manufacturing base.

Key findings

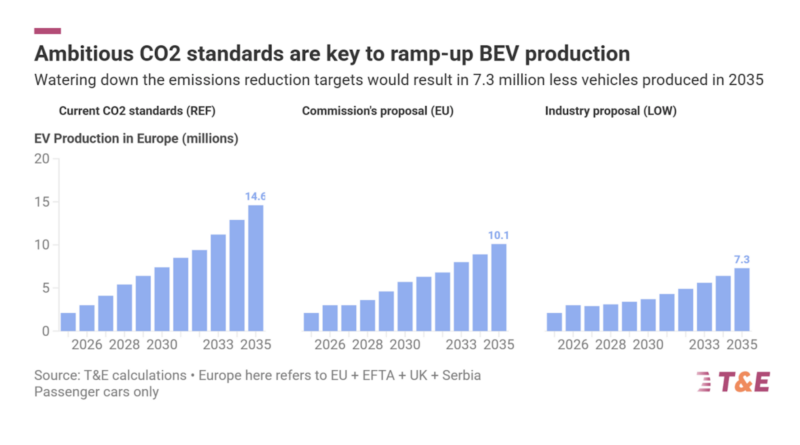

- BEV production will halve compared to today’s projections in 2030 if the auto industry amendments are adopted. The BEV production will reduce from 7.4 million to 3.7 million in 2030 in the LOW scenario, while the Commission proposal will result in a cut of 23% down to 5.7 million units.

- The auto industry amendments will reduce BEV production in 2035 by over 7 mln units. While Europe would produce around 15 million BEVs with current policies in 2035, the Commission proposal would reduce this to 10 million BEVs, while the industry amendments would cut it to 7 million.

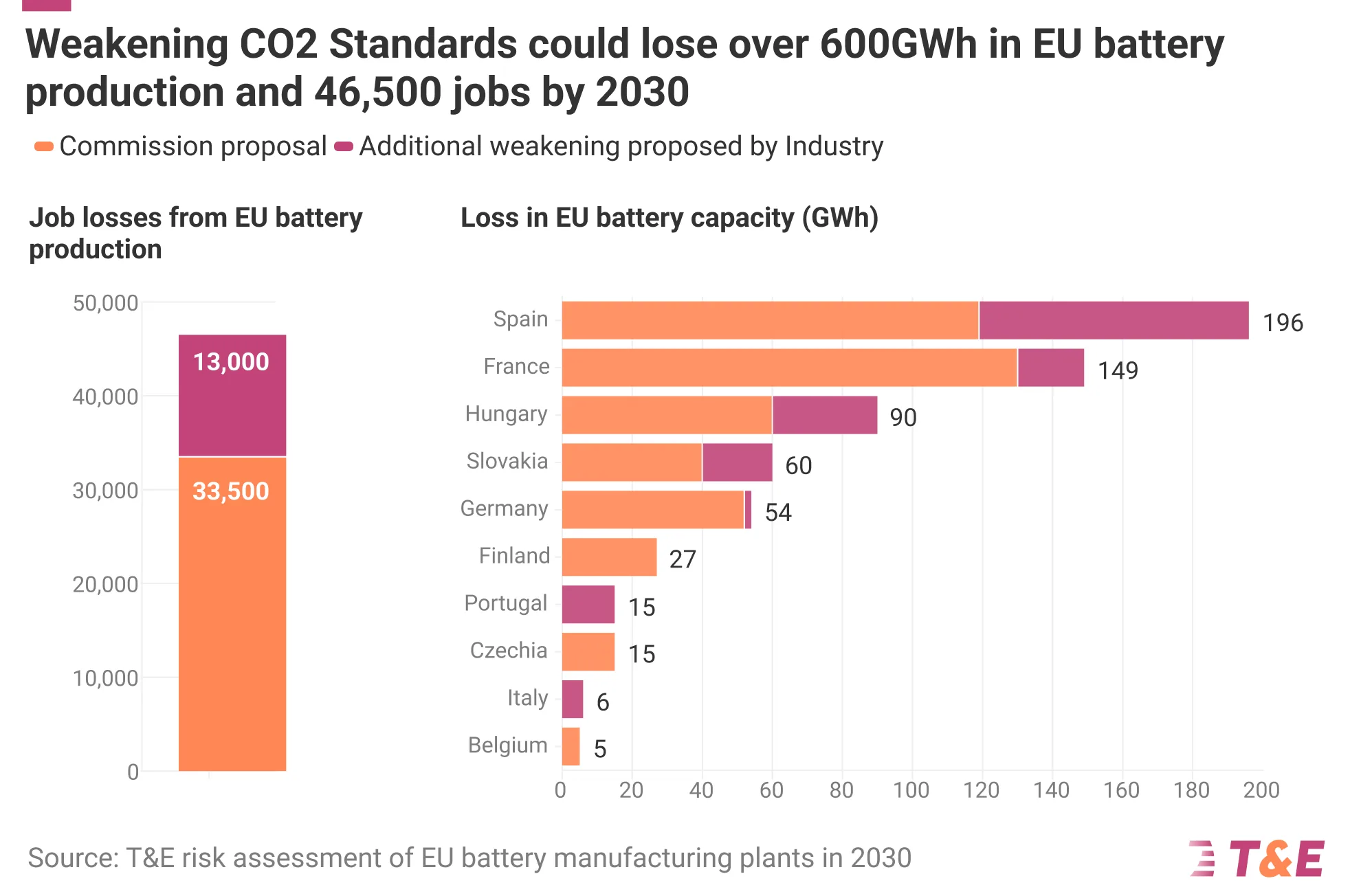

- Over 34 Northvolt-sized battery factories will not be built in 2030 if the auto industry amendments are adopted, resulting in up to 47k jobs lost. The current name-plate capacity of all battery plants will reduce by 56% — to 632 GWh — in 2030 under the Commission’s proposal scenario, equivalent to 21 Northvolt-sized factories. Only 29% of the announced factories will come online in the industry scenario, a significant loss of 1,024 GWh.

- Significant reductions in 2030 capacity are seen throughout the battery value chain. E.g. local manufacturing of cathodes, battery’s most valuable component, could cover over two-thirds of local needs by 2030 if strong car CO2 rules and industrial policy is in place. If the auto industry amendments go ahead, only 5 projects are likely to remain, covering just over 10% of the projected 2030 demand.

- €50 billion could be wasted on oil imports if industry amendments are adopted. Over 2 bln barrels of oil can be avoided by 2035 with ambitious Car CO2 targets, while the battery dependency is a mere 7% compared to the 96% for oil, as industrial policies make it possible to produce batteries and recycle their materials domestically.

This shows that the 2030 Car CO2 target is critical to EV cleantech investment certainty across Europe. Put bluntly, 5-year averaging as proposed by automakers would kill the business case for batteries and their critical components. To ensure factories are built and critical technology is onshored, the EU should keep the 2030-2035 targets unchanged. In addition, strong local content requirements without loopholes (no small BEV should be called Made in EU if it uses a Chinese battery) must be swiftly adopted in the IAA.

To find out more, download the report.

Article from T&E.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News! Advertisement Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here. Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent. CleanTechnica uses affiliate links. See our policy here.CleanTechnica's Comment Policy

Share this story!

Схожі новини

‘Heavy’ hearts as residents of Wang Fuk Court’s only spared block return again

Автомобільний міст на Буковині за 171 мільйон "полегшили" на 2,5 мільйона гривень

Автомобільний міст на Буковині за 171 мільйон "полегшили" на 2,5 мільйона гривень