Critical Minerals: China’s Grip, America’s Volatility, Europe’s Choice

Chatgpt generated image of Europe navigating between China’s processing choke point and America’s federal volatility toward a more resilient battery minerals future.

April 27, 20262 hours

Michael Barnard

0 Comments

Support CleanTechnica's work through a Substack subscription or on Stripe.

Chatgpt generated image of Europe navigating between China’s processing choke point and America’s federal volatility toward a more resilient battery minerals future.

April 27, 20262 hours

Michael Barnard

0 Comments

Support CleanTechnica's work through a Substack subscription or on Stripe.

The energy transition will not fail because the world runs out of useful minerals. It can be slowed, made more expensive, and made more fragile because the industrial systems that turn minerals into batteries, motors, power electronics, grid equipment, and vehicles are concentrated, politically exposed, and hard to rebuild. That is the useful starting point for any serious conversation about critical minerals. The question is not whether the planet contains enough lithium, copper, nickel, cobalt, graphite, manganese, phosphate, rare earths, and other useful materials. The question is who can mine them, refine them, process them, turn them into components, move them through trusted supply chains, and deliver them into bankable factories at the right price and time.

Having been asked to share my perspective on this in an upcoming presentation, synthesizing my various published perspectives and extending the implications through 2035 became a useful activity. For those who want bite-sized content, I would recommend stopping reading here, or maybe just looking at the graphics.

The West now faces two strategic risks at once. China controls a large share of the industrial middle of the battery, magnet, and critical minerals value chains. The United States remains powerful, wealthy, and technically capable, but its federal government can no longer be treated as a stable anchor for allied industrial strategy. That combination matters. Europe, Canada, Australia, Japan, South Korea, and other partners are not designing supply chains in a world where Washington is the obvious center of gravity. They are designing supply chains in a world where China has leverage and the United States has become a high-capability, low-reliability partner.

This is not a reason to slow electrification. It is a reason to do electrification with industrial discipline. Batteries, grids, EVs, storage, renewables, and electric industry remain the practical route away from fossil fuel dependence. But they require materials, processing, factories, trained workers, permits, finance, standards, recycling and trust. China built much of that system first. The West is now trying to rebuild enough of it to reduce coercion risk without slowing the transition it needs.

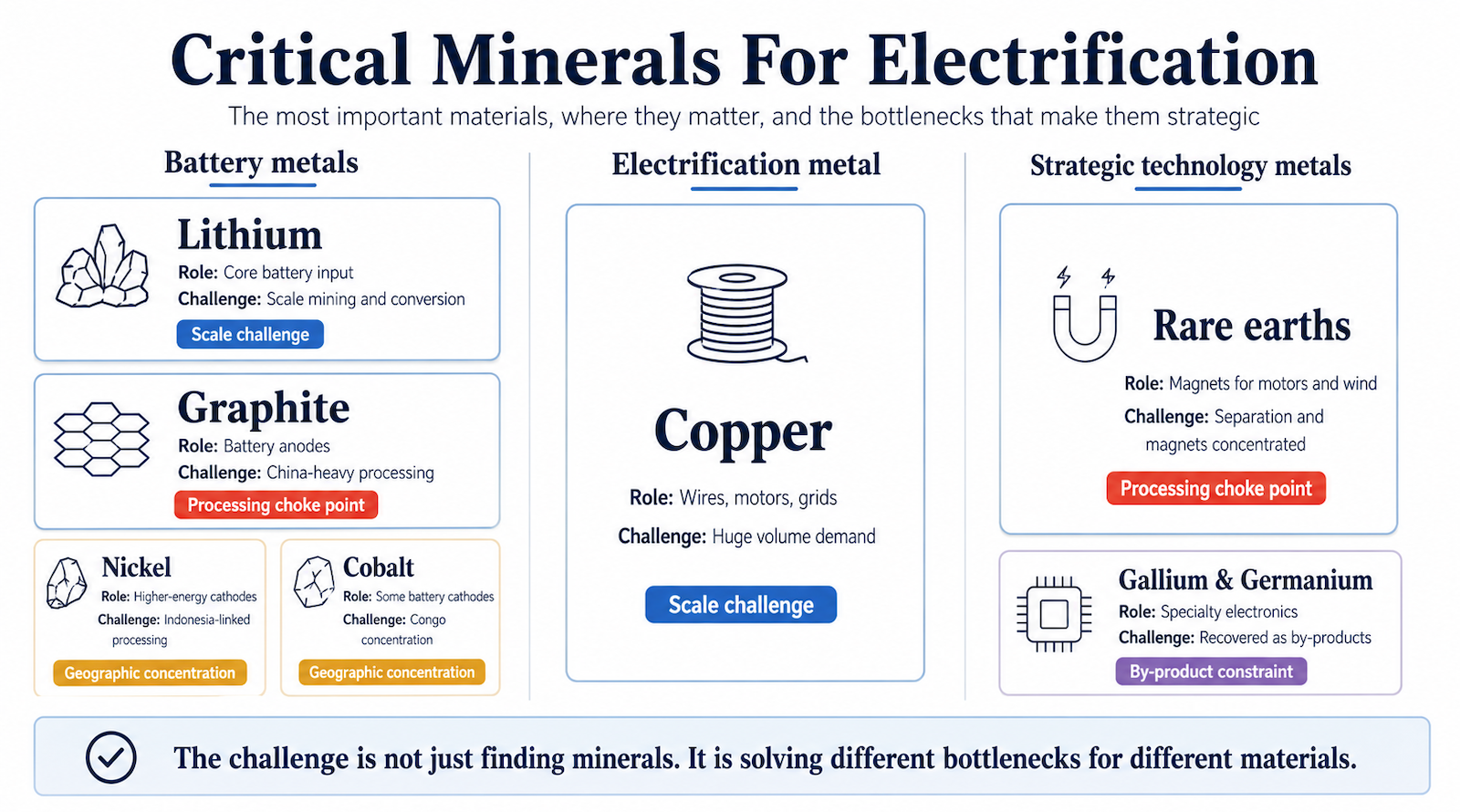

The International Energy Agency’s critical minerals work has made the outside view clear. Demand for lithium, graphite, nickel, cobalt, copper, manganese, rare earths, and related materials rises in every serious electrification scenario, but the constraint is not the same for each mineral. Lithium is not cobalt. Cobalt is not graphite. Graphite is not copper. Rare earth mining is not rare earth separation. Nickel ore is not battery-grade nickel sulphate. A domestic mine is not the same as a secure supply chain. The supply chain step matters as much as the element.

Resources, reserves, production, and bankable supply are different categories. A resource is what geologists know or expect to exist. A reserve is the portion that can be extracted under current economics and technology. Production is what operating mines and processing plants deliver this year. Bankable supply is narrower again. It requires the right purity, the right chemical form, the right transport links, the right permits, the right customers, the right cost structure, and the right political risk profile. Mineral panic often starts by confusing those categories, then turns the confusion into a dramatic forecast.

Director of the British Geological Survey’s Critical Minerals Intelligence Centre Gavin Mudd’s framing is useful because it separates geological abundance from industrial delivery. The world has large mineral resources. That does not mean every deposit becomes a mine. It also does not mean today’s reserves define tomorrow’s limits. Reserves expand with exploration, prices, technology, and demand. They contract when prices fall, projects fail, social license is lost, or governments create risk. The mineral system is dynamic. Forecasts that freeze today’s reserves, today’s battery chemistries, today’s recycling rates, and today’s demand patterns are weak guides to a 2035 industrial system.

This is where many scarcity narratives go wrong. They treat the future as a scaled-up version of a static present. They assume that battery chemistries do not shift, recycling remains marginal, demand follows fossil primary energy rather than useful energy services, and engineers do not substitute around cost and supply problems. That is not how industrial systems behave. The last decade of batteries is already evidence. Cobalt intensity fell. LFP scaled. Pack design improved. Sodium-ion entered commercial production. Automakers and battery firms changed recipes because price, performance, safety, and supply chains pushed them to change.

The old mineral doom story was that cobalt would stop electric vehicles. The concern was not invented. The Democratic Republic of Congo dominated mine supply, China dominated refining, artisanal mining raised ethical issues, and cobalt-heavy chemistries were common in early EV packs. The conclusion was wrong. Battery makers reduced cobalt content, shifted to LFP where energy density was less critical, improved procurement controls, and diversified chemistry choices. Cobalt remains an important and messy mineral, but it is not the master constraint on electrification that many assumed in the 2010s.

Nickel followed a related path. High-nickel chemistries are valuable where range, weight, and energy density matter, but they are no longer the whole EV future. Indonesia’s rise in nickel production and China-linked processing has created environmental and geopolitical exposure, but LFP reduced nickel’s leverage over mass-market vehicles and stationary storage. That is what chemistry substitution does. It does not remove mineral exposure. It changes the exposure.

Lithium is a different case. Batteries still need lithium in most high-volume chemistries, and the IEA’s 2025 outlook points to lithium as one of the materials where announced mined supply falls short of projected 2035 primary supply requirements under current policies. But that is not the same as saying the world lacks lithium. It means the current project pipeline, price environment, permitting process, chemical conversion capacity, and financing are not enough on current settings. Lithium’s problem is supply chain delivery, not the absence of atoms.

Graphite is less discussed than lithium but may be one of the sharper Western exposures. LFP reduces nickel and cobalt risk, but anodes still matter. Natural graphite mining can be diversified, but battery-grade spherical graphite processing is a specialized industrial step. Synthetic graphite can be produced outside China, but it requires energy, capital, and process competence. China’s role in graphite processing and anode supply means that even a cobalt-free, nickel-free LFP battery can still carry China-shaped exposure. That is the type of problem public debate often misses because it is less dramatic than lithium panic.

Copper is broader than batteries and may be more important to electrification as a whole. EVs need chargers. Chargers need distribution systems. Wind and solar need interconnections. Data centers need substations. Heat pumps, industrial electrification, and grid upgrades need wires, transformers, switchgear, and motors. Copper mines have long lead times, declining ore grades, and large capital requirements. The IEA has pointed to copper as one of the more difficult 2035 supply challenges on current project pipelines. Substitution with aluminum can help in some uses, but copper remains one of the metals that turns electrification from a concept into infrastructure.

The byproduct metals are a different class again. Gallium, germanium, indium, tellurium, and selenium are often produced as byproducts of larger host-metal industries. If demand for gallium rises, the world does not open a gallium mine in the normal sense. It depends on how much bauxite, zinc, copper, or other host material is mined and processed, and whether recovery systems capture the byproduct. That makes these materials less responsive to price signals than primary metals. They are also better candidates for targeted stockpiles because volumes are smaller and strategic effects can be large.

This is the mineral discrimination that strategy requires. Lithium may need more mines, brines, processing, and recycling. Copper may need grid planning, substitution, mine investment, and demand efficiency. Graphite may need anode processing outside China. Gallium and germanium may need recovery systems and stockpiles. Rare earths may need separation, and magnet manufacturing more than another press conference about a deposit. Each material has its own bottleneck. A useful strategy starts by naming the bottleneck, not by declaring a general mineral emergency.

China understood the value chain before the West remembered that value chains exist. It did not dominate critical minerals because it owned every deposit. It built capacity across mining relationships, refining, chemical processing, rare earth separation, anodes, cathodes, cells, packs, manufacturing equipment, and customer demand. It supported firms, tolerated low margins where scale mattered, trained workers, built clusters, and learned by doing. China treated critical minerals as industrial infrastructure. Much of the West treated them as low-cost procurement.

That difference now matters. China has leverage because it controls many middle layers of the system. It does not need to shut everything off. A license requirement, a delay, a signal that exports may be constrained or a period of price suppression can change investment decisions. If a Western graphite processor or rare earth separator needs a higher price to survive, China does not need to win a war. It can use scale and pricing to make the Western project unfinanceable. If a Western automaker cannot verify non-China battery inputs, a tax credit may disappear. If a defense contractor needs magnets, a small material flow can become a large strategic issue.

China does not need to be treated as an enemy for its dominance in critical minerals, but should be treated as a strategic risk. China did what serious industrial states do: it identified a set of technologies that would matter, invested across the value chain, built processing capacity, trained workers, supported firms, tolerated long learning curves, and created manufacturing ecosystems the rest of the world now depends on. That is competence, not villainy. But competence at that scale creates leverage. When one country holds dominant positions in refining, chemical processing, graphite anodes, cathode precursors, rare earth separation, magnets, and battery manufacturing equipment, other economies have to ask what happens if trade frictions, export controls, diplomatic disputes, price manipulation, or domestic Chinese priorities interrupt supply. The answer is not panic, decoupling, or moral theater. It is strategic derisking.

The useful Western strategies are clear. Diversification reduces dependence on one country at vulnerable stages. Friendshoring builds supply with countries that have resources, energy, skills, and political alignment. Recycling turns today’s deployed batteries, electronics, motors, and grid equipment into future supply. Chemistry substitution reduces exposure where performance allows. Targeted stockpiles cover small-volume, high-consequence chokepoints. Processing capacity rebuilds the missing middle between mines and factories. Bankable offtake gives projects customers, not just applause.

The weak strategies are also clear. Full decoupling from China is not a plan. It is a fantasy unless the West accepts higher costs, slower deployment, and years of gaps. Tariffs can buy time only if they support real plants, real contracts, and real performance milestones. Domestic mining can help, but not every mine is strategic. A mine is strategic only if it addresses a real chokepoint, has environmental and community legitimacy, connects to downstream processing, and can deliver on a relevant timeline. Otherwise it is domestic in geography and decorative in strategy.

The United States still matters to this story. It has enormous advantages: capital markets, universities, national labs, defence procurement, large energy demand, strong firms, state industrial competition, skilled workers, large vehicle markets, and deep engineering talent. The Inflation Reduction Act, 45X manufacturing credits, Department of Energy loan programs, battery materials processing grants, and defense procurement have all shifted real money toward batteries, materials, recycling and selected strategic minerals. The US can build factories, finance projects, create demand, and move quickly when incentives line up.

But the credible American strategy is no longer a Washington strategy. It is distributed across states, utilities, firms, defense procurement, public power agencies, national labs, and private offtake contracts. That distinction is now central. The federal government can provide useful money and contracts in one year, then become a source of tariff risk, policy reversal, and demand destruction in the next. Allies and investors cannot treat federal continuity as the base case.

The US is a high-capability, low-reliability partner. That is not a moral judgment. It is a planning assumption. Allies have watched federal policy swing across administrations, with clean energy incentives created, challenged, narrowed, defended, and attacked. They have watched tariff threats and trade wars hit allies. They have watched decarbonization support coexist with attacks on wind, solar, EVs, and climate policy. They have watched agreements treated as bargaining chips. A 15-year lithium refinery, graphite anode plant, or rare earth separation facility does not finance well on the assumption that Washington will stay coherent for 15 years.

Gallup’s 2025 polling captured part of this trust problem. US leadership approval among NATO countries fell to about 21%, while European Union leadership approval among NATO members was around 60%. In global approval polling, China edged ahead of the U.S. in 2025, around 36% to 31%. Polls are not industrial policy, but they indicate the credibility problem allies must price into decisions. The issue is not whether US institutions can do useful things. They can. The issue is whether the federal government can be treated as a stable load-bearing beam in a long-term allied minerals system. It cannot.

The political calendar reinforces that point. As of April 2026, generic congressional ballot averages such as Nate Silver’s showed Democrats ahead by roughly 6 points, making a House flip a serious planning case. A Senate flip is harder because of the starting seat count and map, but it is possible enough to affect expectations. The 2028 presidency is a high-change event by design because Trump cannot serve another term under the 22nd Amendment. Even if Republicans retain the White House, it will be a new administration. If Democrats win, another federal reset follows. Critical minerals projects cannot assume continuous federal alignment across that period.

The durable US strategy has to be built from the bottom up and the middle out. It lives in states, utilities, public power agencies, grid operators, automakers, battery manufacturers, storage developers, ports, national labs, universities, regional banks, defense procurement, and private offtake. Federal policy can help, but it should be treated as useful when converted into contracts and dangerous when left as rhetoric.

The evidence for this distributed strategy is already visible. The US Energy Information Administration expects large additions of utility-scale generation capacity in 2026, with solar, battery storage, and wind dominating planned additions. That reflects developers, utilities, interconnection queues, state markets, and economics, not just federal ambition. Battery storage is now a grid reality. Utilities procure it because it solves capacity, ramping, congestion, and reliability problems. Public power agencies and regulated utilities can create demand for batteries even when Washington argues with itself.

States also matter because they control many practical parts of industrial buildout. They can support sites, roads, ports, workforce programs, permitting, training colleges, local tax packages, power supply, and regional clusters. Georgia, Michigan, Nevada, Tennessee, Texas, California, the Carolinas, and others do not all have the same politics, but many have reasons to build battery, storage, auto, grid, or mineral processing capacity. Some want jobs. Some want manufacturing. Some want grid reliability. Some want clean energy. The motive can differ while the industrial outcome converges.

This distributed US model is not as elegant as a national strategy. It is, however, more credible. A battery storage procurement by a utility, a 10-year offtake contract by an automaker, a state-backed anode cluster, a Department of Defense magnet contract, a DOE loan that has closed, or a port infrastructure investment has more strategic value than a federal speech about critical minerals. The US should be judged by what becomes contractual, financed and under construction, not by what is announced.

Federal instruments still have a role, but it is narrower. The Department of Defense is credible where the material is tied to national security and the contract is real. The MP Materials deal, with long-term offtake and a price floor for rare earth materials and magnets, is the kind of action that changes bankability. It combines a true chokepoint, a buyer, price support, and a production pathway. That is different from broad claims about domestic mining. The U.S. government can still support rare earths, graphite, lithium processing, defense-critical materials, and grid resilience when it uses procurement, price floors, loans, and contracts.

The Department of Energy can also matter when it turns grants, loans, and tax credits into operating assets. The 45X Advanced Manufacturing Production Credit and battery materials processing grants can shift economics for cells, modules, critical minerals, and components. But the lesson is to close deals and build projects before politics changes. A tax credit that survives long enough to create a plant is useful. A tax credit that becomes a campaign target before financing closes is a risk factor.

The decentralized US strategy should focus on durable actors and real chokepoints. States should compete for processing, anodes, cathodes, recycling, grid storage, and industrial clusters, not just cell assembly. Utilities and public power agencies should use long-term storage procurement to support low-risk chemistries and domestic or allied supply where reasonable. Automakers and storage developers should sign offtake for lithium chemicals, graphite, cathode precursors, and recycled materials. Defense procurement should focus on rare earths, magnets, graphite, and other true security materials. Federal finance should turn support into contracts and closed loans. Tariffs should be ignored as strategy unless they support financed capacity with performance milestones.

This changes how allies should engage with America. They should not treat “the United States” as one actor. California is not the same counterparty as the White House. A Texas grid storage developer is not the same as a tariff announcement. The Pentagon is not the same as campaign rhetoric. A signed offtake agreement with an automaker is not the same as a federal policy speech. Europe, Canada, Australia, Japan, and South Korea should work with the American institutions that can deliver and design around the ones that can reverse.

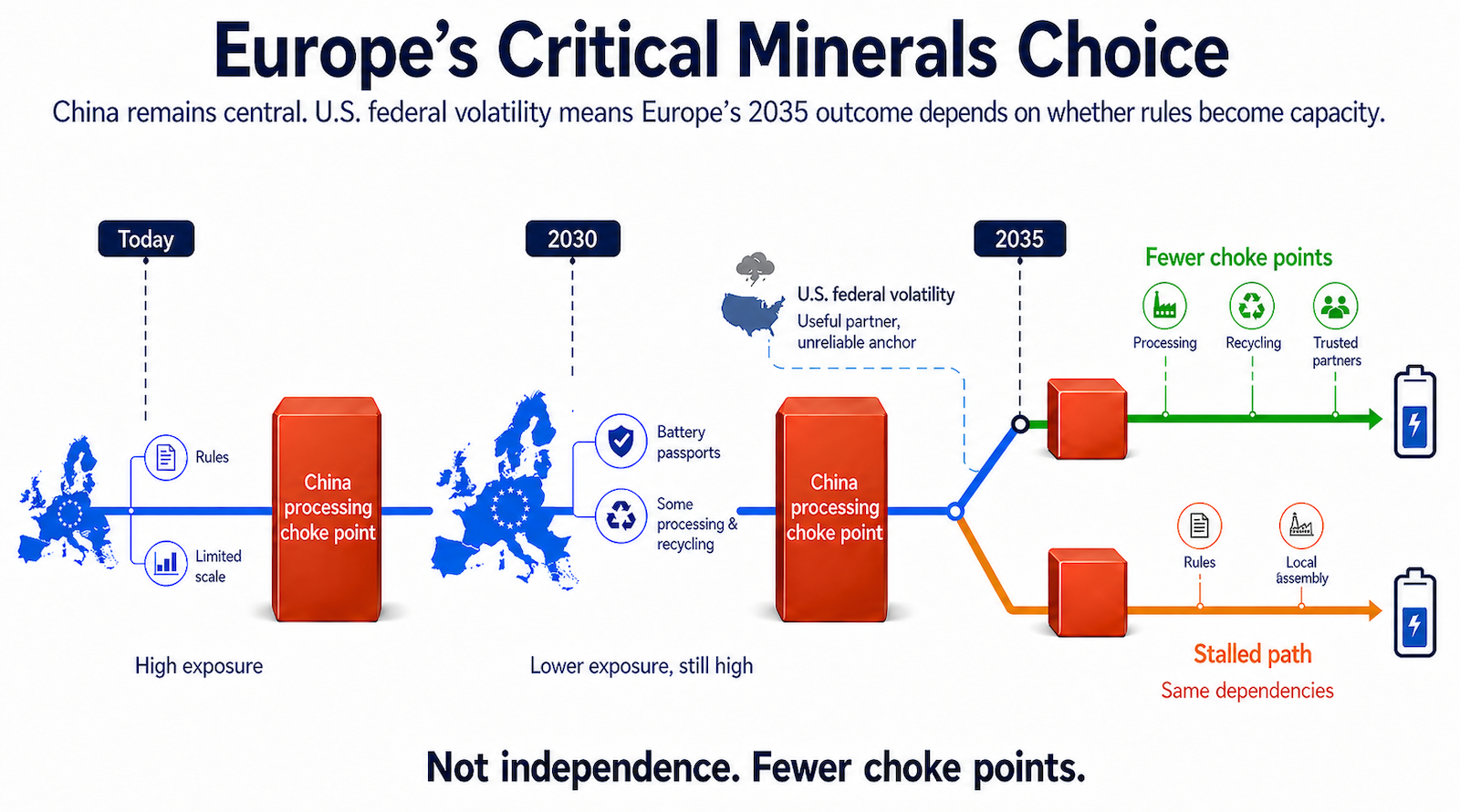

Europe’s strategy has to be built in the space between Chinese industrial strength and American federal volatility. Europe cannot outscale China across the whole battery minerals value chain by 2030 or 2035. It also cannot assume that Washington will anchor a durable allied response. Europe’s task is to build a premium, circular, standards-based and friendshored battery minerals system that can cooperate with credible American institutions without depending on federal US continuity.

Europe has the more coherent policy architecture. The European Critical Raw Materials Act sets 2030 benchmarks of 10% domestic extraction, 40% processing, 25% recycling, and no more than 65% dependence on a single third country for any strategic raw material at a relevant processing stage. Those numbers matter because they show a diversification strategy rather than a claim of independence. Europe is not saying it will mine everything at home. It is saying it needs extraction, processing, recycling, and supplier diversity in measured shares.

The 40% processing target is more strategic than the 10% extraction target. Europe can miss some domestic mining ambitions and still improve its position if it builds refining, separation, precursor, anode, cathode, and recycling capacity. Processing is where China’s leverage is strong. It is also where Europe can turn market access, standards and carbon constraints into industrial policy. A European refinery using higher-cost energy and stricter environmental rules may not match Chinese benchmark prices. If it provides resilience, traceability, and lower-carbon supply, the price gap is not a surprise. It is the security premium made visible.

Europe’s Battery Regulation is one of the more mature policy tools in this space. It requires battery passports, carbon footprint disclosure, due diligence, material recovery, and recycling targets. By the end of 2027, European rules require high recovery rates for cobalt, copper, lead, and nickel, with lithium recovery starting lower and rising. By the end of 2031, targets rise again, including 80% lithium recovery. Those rules will not create a large end-of-life EV battery stream by 2030 because most of the first large EV cohorts will still be in use. But they build the regulatory and industrial base for 2035, 2040, and beyond.

That is Europe’s main strength. It can make compliance part of market access. Battery passports, recycled content, embedded carbon, and due diligence can shape global supply chains because suppliers want access to the European market. This is regulatory power used as industrial policy. It will not make Europe the lowest-cost battery region. It can make Europe the world’s premium, traceable, circular battery market if the rules connect to real processing and recycling capacity.

Europe’s risk is that it becomes excellent at regulating supply chains it does not control. Northvolt’s collapse was a warning. Battery manufacturing is not created by policy architecture alone. It requires process engineering, yield, supplier networks, working capital, operational discipline, and scale. Europe has expensive energy, slow permitting, local opposition to mines and industrial facilities, and less tolerance for the hard middle of industrial buildout. It has a coherent framework, but it still has to convert that framework into factories, refineries, recycling plants, offtake contracts, and trained workers.

The Raw Materials Mechanism should become a bankability engine, not just a matchmaking platform. Demand aggregation is useful, but projects need price floors, contracts for difference, pooled purchasing, storage contracts, and credit support. If Europe wants secure, traceable, non-coerced, lower-carbon supply, it has to pay for it. The premium should be explicit. Secure supply is not the same product as the cheapest ton available in a China-shaped market.

Europe should also support price benchmarks for secure critical minerals. Chinese-linked benchmark prices can make Western projects unfinanceable if they do not reflect carbon, security, labor, traceability, or coercion risk. A European or allied benchmark for certified material would not eliminate the cost gap, but it would make the value proposition visible. Investors can finance a premium market with rules and customers. They cannot finance sentiment.

Battery passports should become a bridge between regulation and capacity. If batteries entering Europe must document carbon footprint, material origin, recycled content, and due diligence, European recyclers, refiners, anode makers, and cathode producers should receive support to serve that compliant market. Otherwise the passport becomes paperwork wrapped around imported capacity. The policy goal should be to make compliance a demand signal for European and allied industrial buildout.

Europe should accept Asian battery firms under conditions that serve European strategy. Excluding Chinese, Korean, and Japanese expertise would slow learning and raise costs. Process competence matters. But market access can come with requirements for local workforce training, recycling integration, data protection, material transparency, local suppliers where practical, and progressive localization of higher-value steps. Europe does not need battery autarky. It needs leverage, learning, and resilience.

Europe should also deepen partnerships that do not depend on Washington. Canada has minerals, clean electricity, mining expertise, and proximity to US markets. Australia has mineral supply and a clearer role if it moves further into processing. Japan and South Korea bring battery, materials, and manufacturing competence. Chile and Brazil have resource depth and can capture more value if partnerships are structured well. South Africa, Namibia, and selected African partners can matter where projects include local value creation rather than another round of extraction-only development. Norway and the United Kingdom can contribute through energy, finance, offshore competence, standards, and niche industrial capacity.

This architecture does not require excluding the United States. It requires treating the United States as a set of counterparties rather than a single reliable actor. Europe should work with US states, utilities, automakers, storage developers, defense-linked procurement offices, public power agencies, national labs, and finance institutions where projects are real and contracts are durable. It should not make US federal consistency the load-bearing assumption.

The transatlantic strategy should reflect that. The old idea was an allied critical minerals market led by Washington and Brussels. The better idea is a modular allied minerals market that can survive Chinese coercion and American volatility. That sounds less tidy, but it is closer to the world investors and allies face. It allows US participation without making US federal continuity the central assumption.

One part of the system should be Europe-led standards: battery passports, carbon disclosure, recycled content, due diligence, and traceability. One part should be North American, if the US repairs trust with Canada and Mexico and stops treating them as tariff targets. One part should be Indo-Pacific, with Australia, Japan, South Korea, and selected Southeast Asian partners. One part should be resource partner finance, with Chile, Brazil, South Africa, Namibia, Indonesia, and others where geology, governance, and local value creation can line up. One part should be defense and strategic stockpiles, focused on small-volume materials with large security consequences.

This system does not require excluding China from everything. That would be costly and slow. It requires reducing the ability of China to veto critical supply. There is a difference. Chinese firms may still sell batteries, equipment, materials, and technology into global markets. But Europe, the US and partners need at least one credible non-coerced route for every strategic node: graphite anodes, lithium chemicals, cathode precursors, rare earth magnets, selected battery components, recycling, and key grid materials. The goal is not purity. It is resilience.

By 2030, the global battery minerals market will be much larger and still China-centered. The IEA’s Global EV Outlook 2025 expects EV battery demand to exceed 3 TWh in 2030, up from roughly 1 TWh in 2024. Global cell manufacturing capacity is growing, and China’s share may fall from about 85% in 2024 toward roughly two-thirds by 2030 if committed projects proceed. That is visible diversification, not strategic autonomy.

Europe and the US will both have more battery factories by 2030. The US may have more cell and pack capacity because of tax credits, state competition, and large private markets. Europe will have stronger rules, more recycling capacity, battery passports, and some processing projects. Both will remain exposed to China or China-linked supply for graphite, anodes, cathode precursors, processing equipment, rare earths, and some refined battery chemicals. A local battery factory supplied by imported anode material and cathode precursors is better than importing the whole pack, but it is not full strategic control.

Chemistry will do meaningful work by 2030. LFP will remain central in EVs and stationary storage. Sodium-ion will likely find roles in stationary storage, lower-cost mobility, and applications where weight and volume matter less. High-nickel chemistries will persist where energy density pays. Cobalt intensity will keep falling in mass-market batteries. The battery industry will keep routing around some mineral constraints because chemistry is a design space, not a fixed menu.

Recycling in 2030 will be important but not large enough to replace primary supply. Manufacturing scrap, warranty returns, and early end-of-life batteries will feed recyclers, and black mass processing will grow. But most EV batteries from the first large adoption waves will still be in use. The value of recycling policy before 2030 is preparation. It builds collection systems, standards, plants, recovery technologies, customer relationships, and quality controls before the major end-of-life wave arrives.

By 2035, the test becomes harder. Recycling volumes grow. Sodium-ion has had time to settle into its practical markets. LFP is mature. Cobalt is less central than old panic narratives assumed. Lithium remains critical, and copper remains a broad electrification constraint. Graphite and rare earths remain strategic if non-China processing and anode or magnet capacity have not been built at scale. The IEA’s 2025 outlook indicates that lithium and copper face more serious 2035 supply gaps on current project pipelines than nickel or cobalt, while graphite and rare earths remain exposed because of concentration.

The 2035 question is whether the West built real supply chains or only announced capacity. A gigafactory without secure inputs is not enough. A mine without refining is not enough. A tariff without production is not enough. A standard without industrial capacity is influence, but not control. Europe’s 2035 position depends on whether it turned regulation into bankable demand and processing capacity. America’s 2035 position depends on whether its states, utilities, firms, defense buyers, and finance institutions built durable capacity despite federal volatility.

The right goal is not mineral independence. That phrase invites bad policy. No large industrial economy is independent of global supply chains. The right goal is coercion-resistant electrification. That means enough diversified supply, enough friendshored processing, enough chemistry substitution, enough recycling, enough targeted stockpiles and enough trusted demand that no single country can halt the transition by squeezing one node.

The harder version is that the supply chain must now be resilient to both Chinese leverage and American federal volatility. China is the strategic external supplier with processing power. The US is the powerful partner whose federal government cannot be treated as stable enough to anchor the system. Europe and other allies should work with the parts of America that can deliver, but build systems that survive the parts that cannot. Strategy starts with the world as it is, not the world that would make planning easier.

The next decade is not about finding enough rocks. It is about rebuilding the industrial capacity and international trust required to turn rocks into electrification.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News! Advertisement Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here. Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent. CleanTechnica uses affiliate links. See our policy here.CleanTechnica's Comment Policy