China’s Electric Concrete Mixer Boom Is A Warning To Slow Heavy Truck Markets

Infographic of electric concrete trucks by author with ChatGPT

May 8, 202621 minutes

Michael Barnard

0 Comments

Support CleanTechnica's work through a Substack subscription or on Stripe.

Infographic of electric concrete trucks by author with ChatGPT

May 8, 202621 minutes

Michael Barnard

0 Comments

Support CleanTechnica's work through a Substack subscription or on Stripe.

Battery-electric concrete mixers are becoming one of heavy transport’s more interesting electrification stories, not because they are glamorous, but because they are difficult-looking vehicles that are proving easier to electrify than many expected. In China, they have moved from niche to major new-sales category in five years. Outside China, they remain mostly first trucks, trials, and small fleets. That contrast matters because it separates a proven technical pathway from broad global replication. Every municipality, policy maker, transportation strategist and concrete truck fleet operator should be paying attention to what’s happening in China.

People often say “cement truck,” but the relevant vehicle is usually a ready-mix concrete mixer. Cement is one ingredient in concrete. The truck carries wet concrete from a batching plant to a construction site while rotating the drum to keep the mix workable. A battery-electric concrete mixer electrifies the truck drivetrain, and usually the drum operation as well. Battery-swapping concrete mixers belong in this category because the truck is still electric.

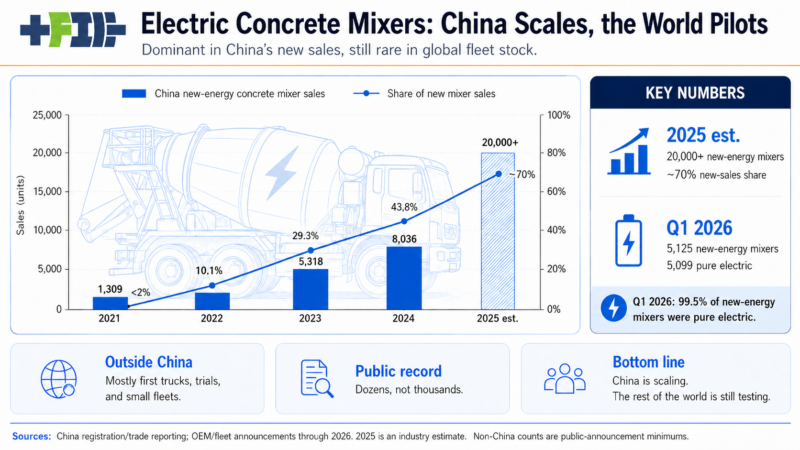

China is the center of the story. In 2021, China sold 1,309 new-energy concrete mixers, with penetration under 2% of new mixer sales. In 2022, sales rose to 2,152, with penetration at 10.1%. In 2023, sales reached 5,318, with penetration at 29.3%. In 2024, sales reached 8,036, and penetration rose to 43.8%. A 2025 industry estimate put sales above 20,000, with penetration heading toward about 70%. That is the shift from demonstration to mainstream procurement.

The first quarter of 2026 sharpened the point. China reported 5,125 new-energy concrete mixer sales in Q1 2026. Of those, 5,099 were pure electric with the other 26 being methanol-electric hybrids. The same reporting showed zero fuel-cell concrete mixer sales in the quarter. That does not mean every mixer on China’s roads is now electric, and it does not mean electric mixers are dominant. Fleet stock turns over slowly. But it does mean that in the only market buying thousands of these vehicles per year, the zero-emission concrete mixer segment is being carried by batteries.

The reason this matters is that concrete mixers look hard to electrify if the only question is weight. They carry dense loads. They work in construction environments. They have delivery windows. They spend time in urban congestion and at job sites. They have to be reliable because a failed concrete pour is expensive. Yet heavy is not the same as hard. The better question is how knowable the work is. Concrete mixers usually operate from fixed batching plants, run local or regional routes, and return to known locations. That makes charging or battery swapping much easier to plan than for random long-haul freight.

A batching plant can become the energy hub. The operator knows where the trucks start, where they return, how long they wait, which routes are short, and which customers create repeatable demand. Charging can be installed at the plant. Battery swapping can be considered where there is enough volume and standardization. Dispatch software can assign electric trucks to suitable routes first, then expand as operators gain confidence. The vehicle may be heavy, but its work is bounded.

China moved first because the pieces lined up. It has domestic heavy truck manufacturers, large battery suppliers, urban air-quality pressure, policy tools, and a construction equipment market large enough to create learning effects. It also has more experience with heavy-duty battery swapping than most countries. Battery swapping is not automatically the right model everywhere, but for high-utilization vehicles returning to industrial nodes, it can reduce downtime if the infrastructure has enough throughput.

That story should not be reduced to subsidies. Subsidies can create bad pilots as easily as good markets. What matters is alignment. Manufacturers can supply the trucks. Batteries are available. Policy creates pressure. Infrastructure can be concentrated around plants and industrial districts. Fleet owners see vehicles working, OEMs improve models, cities gain confidence in diesel restrictions, and procurement shifts. The China data shows not just more electric mixers, but a rising share of new mixer purchases.

The hydrogen contrast is instructive. Hydrogen’s usual heavy-truck claims are range and refueling speed. Those are weaker for a truck that returns to a known plant and performs bounded work. Battery-electric trucks have better energy efficiency, simpler drivetrains, and an easier fuel supply. Fuel-cell systems add hydrogen production, distribution, storage, station complexity, and cost uncertainty. In China’s Q1 2026 concrete mixer data, buyers in the scaled market were choosing pure electric vehicles almost entirely.

Outside China, the market is real but early. Switzerland had early electric mixer deployments through Holcim and Designwerk-Futuricum. The United Kingdom has seen Tarmac and Aggregate Industries move from first-truck announcements to small operating fleets. Germany has CEMEX deployments with Volvo and Putzmeister electric mixers. Norway’s Unicon has reported eight electric concrete trucks in operation. Denmark has one deployed Scania electric mixer and ten more on order. Sweden, Singapore, Hong Kong, Australia, New Zealand, the UAE, and Mexico have all had first deployments, trials, or small announcements. That is geographic spread, but not market dominance.

The language outside China still says a lot. It is mostly “first electric mixer,” “trial,” “commercial pilot,” “small fleet,” and “order.” Those are early-market phrases. Public data is incomplete, as some companies do not announce every vehicle and some trucks are operated by contractors or leasing partners. But even if true deployment is higher than public announcements, the scale is still nowhere near China’s thousands per year.

Compared with electric buses, garbage trucks, and fire trucks, concrete mixers sit in the middle. Buses are the mature case, especially in China, because they are scheduled, depot-based, visible, and politically attractive. Garbage trucks are the operational cousin, with fixed local routes, stop-start work, return-to-depot charging, and strong air-quality and noise benefits. Fire trucks are the harder comparison because they are emergency assets procured for rare worst-day requirements, not average daily utilization. Concrete mixers are commercial productivity assets. Their routes can be studied, their energy use can be measured, and their payback can be modeled.

The economics vary by market, but the structure is clear. Electric mixers usually cost more upfront and require charging or swapping infrastructure. Against that, they displace diesel, reduce fuel-price exposure, lower drivetrain maintenance, reduce brake wear through regenerative braking, and may gain access to low-emission construction zones or public procurement advantages. The right measure is not truck purchase price alone. It is the cost of delivered concrete, including energy, maintenance, uptime, charging, grid upgrades, payload, driver acceptance, and reliability.

Infrastructure is often the gating factor. A plant with a few electric mixers may manage with modest charging upgrades. A plant with dozens may need serious grid capacity, load management, storage, or staged deployment. Battery swapping can reduce vehicle downtime, but it needs standardization, capital, and enough throughput. Subsidizing trucks without enabling plant power is not enough.

Fleet operators should treat early deployments as operating-system pilots, not showroom pilots. The useful questions are which routes work, how much energy the drum requires, how winter and hills affect range, how long trucks dwell at plants, and how charging fits dispatch. A good pilot should teach the company how to buy the next ten trucks, not just how to issue a press release.

Policymakers should draw a similar lesson. The best policy is not a generic statement that heavy trucks should electrify. It is support for the specific duty cycles that are ready. Low-emission construction zones, public procurement requirements, industrial charging support, grid connection reform, construction-site noise rules, and transparent emissions reporting can all shift markets. The China lesson is not that every country can copy China’s exact system. It is that vehicles scale when policy, manufacturing, infrastructure, and operations point in the same direction. Every non-Chinese fleet owner and policy maker should understand that the market test has been run and battery electric won completely. No time should be wasted considering hydrogen for this category of vehicles in other countries.

There are still caveats. China’s figures come from industry and trade reporting, and the 2025 number is an estimate. Non-China data is public-announcement based and should be treated as a lower bound. Construction markets are cyclical. Battery prices, interest rates, electricity tariffs, diesel prices, and grid constraints all affect economics. Battery swapping may not translate to markets without standardization. Some fleets will find that current electric models fit only part of their work.

The signal is still clear. Battery-electric concrete mixers are the strong majority choice in China’s new sales, while the rest of the world is in the early commercial phase. The broader lesson is that “hard to electrify” is often too blunt a label. Some heavy vehicles are difficult because their routes are long, irregular, and poorly served by charging. Others are heavy but predictable. Concrete mixers fall into the second group. They run from known plants, over knowable routes, serving known urban work. The transition will not arrive everywhere at once. It will advance route by route, plant by plant, and fleet by fleet.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News! Advertisement Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here. Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent. CleanTechnica uses affiliate links. See our policy here.CleanTechnica's Comment Policy