BYD Wins In A Slow Return To Normal — China March EV Sales Report

April 22, 20261 hour ago

José Pontes

0 Comments

Support CleanTechnica's work through a Substack subscription or on Stripe.

April 22, 20261 hour ago

José Pontes

0 Comments

Support CleanTechnica's work through a Substack subscription or on Stripe.

After the December end-of-incentive sales rush (NEVs are no longer exempt from purchase tax this year), and the following sales slump, March is signaling a slow return to normal, despite the numbers still being negative.

In March, the overall market was down 15% YoY, to around 1.6 million sales, while BEVs were down by 12% YoY, to 568,000 sales. So, BEVs did better than the overall market. But the PHEV drop was harsher than average (-19%).

Share-wise, March saw plugin vehicles hit 52% market share. This is the same market share as in March 2025. Full electrics (BEVs) alone accounted for 35% of the country’s auto sales, which is already above the 34% score of March 2025.

This result pulled the 2026 share to 45% (in the same period last year, it was at 48% share). BEVs alone were also up, to 28% (30% BEV in Jan–March ’25).

In the overall ranking, the first two months of the year had ICE models populating the top positions, but March is signaling a slow return to normal, with only four ICE models in the top 10.

Rather surprisingly, the Nissan Sylphy ICE model has risen into 3rd place, beating the hot new Li i6. Li Auto’s midsize BEV is currently the best selling new model, though.

Li Auto has had its ups and downs, starting with tremendous success in 2020 thanks to the popularity of its innovative formula — big, comfy SUVs with long-range EREV powertrains. This allowed it to become one of the most successful Chinese startups from the get-go. But around 2024, sales started to suffer. Then, the midsize i6 landed, with unrivaled levels of luxury in the category. The only other successful SUV that could compare to it is the Xiaomi YU7, but that one is sportier than Li Auto’s comfort-focused midsizer, and is generally priced higher than Li’s i6.

So, it seems that Li Auto’s new star player has found its place in the market, and that will allow the startup to ride a second wave of success.

More proof that the market is returning to normal is the fact that BYD placed three models in March’s top 10 — when, in February, it had none.

Looking at the best sellers in several size categories, things are returning to normal, as all but the C segment (compact cars) have plugins leading the way. In fact, the C segment was the only category where ICE vehicles managed to be the majority. This is a recurring topic, as it seems that the C segment is the hardest of all to convert into EVs.

The biggest surprise was the NIO ES8 winning the full size category, beating the Xiaomi YU7 and Fang Cheng Bao Tai 7. Additionally, the Mercedes E-Class ICE model snuck into the silver medal position.

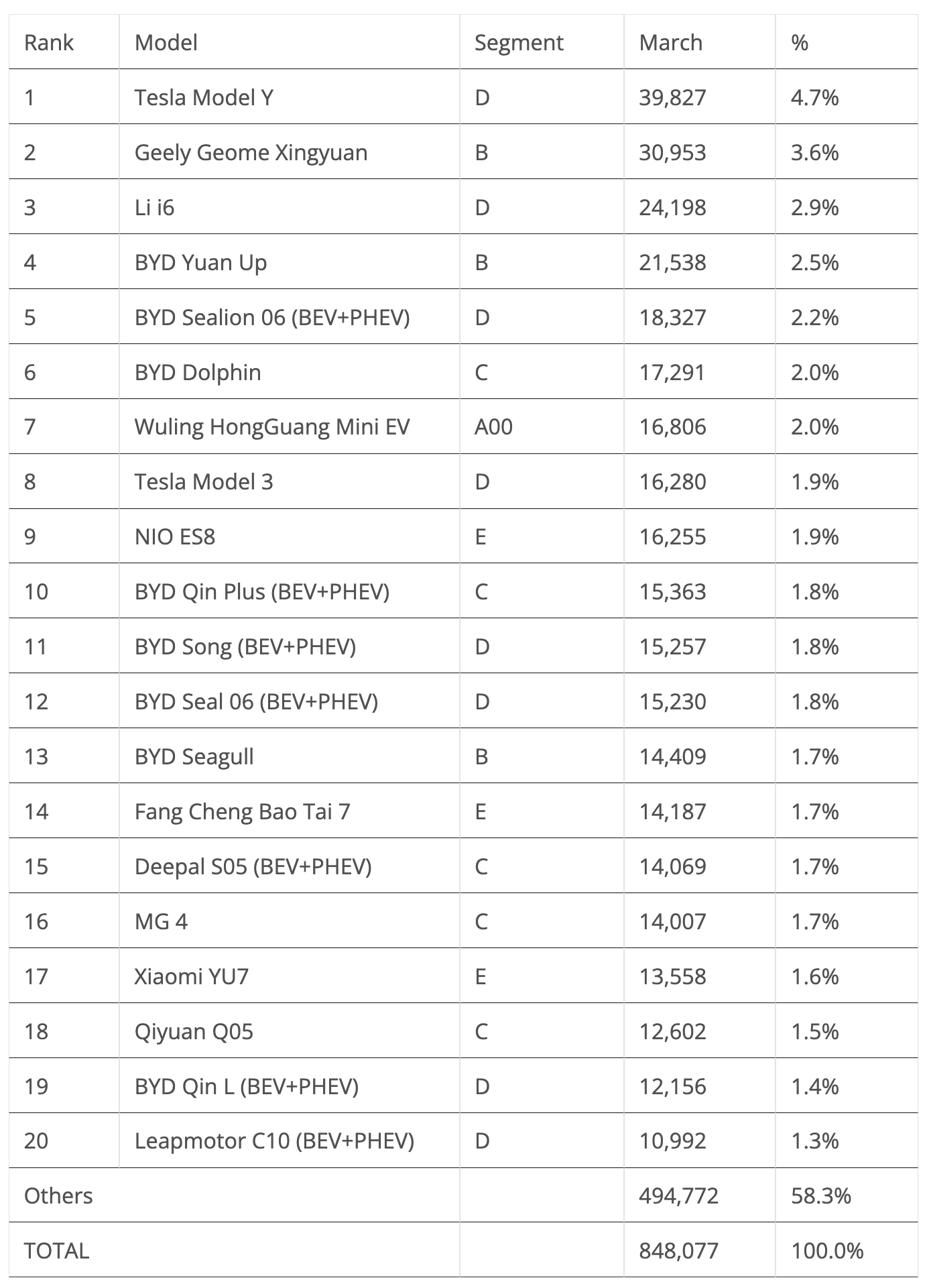

Here’s more info and commentary on March’s top selling electric models:

#1 — Tesla Model Y

The extended wheelbase version, imaginatively called “L,” seems to be helping the Model Y’s fortunes in China. Still, in March, deliveries were down 17% YoY, to 39,827 units. Comparing that with what was going on two years ago, deliveries were also down by 17%. Considering Tesla’s current sales performances, though, the L’s sales can already be considered a win.

#2 — Geely Geome Xingyuan

A BYD Dolphin for BYD Seagull money ($10,000 USD). At least, that’s how Geely’s internal memo might have described the Geome Xingyuan when developing its latest hatchback. And it’s got an interesting name, as Xingyuan translates as “wishing upon a star.” It seems that Geely had its wish granted. The small hatchback has finally given the Hangzhou OEM the much coveted Best Seller status, not only beating its BYD nemesis, but also the rest of the competition. In March, the Geely model was Second, with 30,953 registrations, which represented a 5% drop. With the focus now being in export markets, the small hatchback is now in cruise speed, in its home market.

#3 — Li Auto i6

After a strong start to the year, things continue to go well for the midsize model, with the startup EV securing a podium presence thanks to 24,198 registrations. This was also a new record for the original SUV. With a high level of space, comfort, and luxury for just $35,000 USD (for reference, the cheapest Tesla Model Y in China starts at $36,000 USD), the i6 offers an extensive list of equipment (air suspension, refrigerator, advanced self-driving — including Lidar). It also has a strong focus on space (three-meter wheelbase) and comfort. It’s a model that offers full size luxury in a midsize-priced EV.

#4 — BYD Yuan Up

BYD’s small crossover scored 21,538 registrations, allowing it to reappear in the top 5. With a recent refresh, BYD’s smallest crossover is hoping to steal some of the sales of the Geely Xingyuan superstar. As such, it is positioned at around 75,000 CNY (around $10,500), which sounds cheap until you realize the Geely hatchback’s price starts at 66,000 CNY ($9,400)…. True, the BYD model is a crossover and looks more rugged, but spec for spec, the two are more or less the same. The Geely model is just somewhat cheaper.

#5 — BYD Sealion 06 (BEV+PHEV)

BYD’s new midsize crossover scored 18,327 registrations, allowing it to win another top 5 standing. With the BYD Song going into EV Heaven and the Song L failing to live up to the predecessor’s career, will the Seal 06 be the one to replace the Song on the top of the sales charts? It is positioned at around 150,000 CNY (around $22,000) and has the standard BYD qualities of value for money, design, and connectivity. On the EV specs side, the PHEV version has an above average 27 kWh battery, and the BEV version’s top battery has an unimpressive 79 kWh. Also, the 800V architecture is a plus at this price point. This means that the Sealion 06 has enough value for money to have a good career, but it will be difficult, if not impossible, to repeat the Song’s three-peat title streak (2022, ’23, and ’24), as the competition is increasingly more competitive and the Sealion 06 lacks standout features and specs.

Looking at the rest of the best seller table, let’s see what the highlights show. The Wuling Mini EV returned to the top positions, in this case 7th. The Tesla Model 3 managed a top 10 presence, 8th, despite a 41% YoY sales drop! Meanwhile, the #9 NIO ES8 seems to be the new trendy model in the full size category, ending March in the top half of the table. Not bad for a model that starts at 407,000 CNY ($56,000)…. (Who said all successful Chinese EVs were cheap???)

Another model on the rise is the #15 Deepal S05, Changan’s premium compact crossover, which scored 14,069 registrations. Simlarly, its mainstream cousin, the new Qiyuan/Nevo Q05, hit a record 12,602 registrations, highlighting a positive month for the Chongqing OEM.

Another example of things slowly returning to normal is the fact that there were eight BYDs in the top 20…. And that’s before the new flash charging–capable versions land.

Outside the top 20, the $65,000 Zeekr 9X hit its first five-digit score, 10,060 registrations, with Geely’s Rolls Royce-like SUV looking for another top 20 presence soon. After a long absence from the top positions, GAC’s Aion Y seems to be recovering, with the crossover scoring 8,078 registrations in March, the compact’s best score in a year. Is Aion back in the game?

Looking at the 2026 ranking, the Xiaomi YU7 had a slow month, with fewer than 14,000 units delivered. (Is the waiting list gone?) That meant that the sporty crossover dropped from the leadership position into third. It was replaced in that position by the Geely Xingyuan. The Tesla Model Y also climbed one position, in this case into second.

Below the podium positions, profiting from AITO’s M7 slow month (the model had fewer than 10,000 sales in March), the Li i6 and NIO ES8 climbed one position each, to 4th and 5th, respectively. There were thus five BEVs in the top five positions. A sign of things to come?

The other climbers in the top half of the table belonged to BYD, with the Sealion 06 jumping four positions, into 9th, while the BYD Yuan Up was up to 10th.

In the second half of the table, there were also major movements, with the highlights being the BYD Dolphin going up two spots, now at #13, while two models joined the table — the #17 BYD Seagull is back among the top sellers, while the Deepal S05 is now at #18. Will Deepal’s compact crossover be a regular in the top 20?

Looking at the overall manufacturer ranking, after BYD’s shock crash in the first two months of the year, the Shenzhen make finally rebounded.

Well … sort of. While BYD did regain the top spot, sales were down 38% YoY. That 2nd generation of the Blade battery cannot come soon enough….

Still, eight of the top 10 brands experienced double-digit losses, with the only brand with positive numbers being … Nissan! Nissan was in 7th with a 30% sales increase.

So, if everyone on top is bleeding sales, who is winning?

For this, we need to go outside the top 10 20. #26 NIO was up 122% YoY, to 22,437 registrations, all thanks to the ES8’s success. At #28, BYD’s Fang Cheng Bao is also surging, up 162%. The Tai 7 is providing the majority of the premium brand’s sales. Finally, Geely’s own premium maker, Zeekr, is also on the rise. It was #21 in March, thanks to 22,710 registrations, largely due to the success of the 9X behemoth and the midsize 7X.

Looking at the auto brand ranking, there’s plenty of news. Leader BYD (15.8%, up from 13%) is gaining ground over runner-up Geely (8.3%, down 2.7%). The Shenzhen make is gaining precious ground for the leadership race coming during the remainder of the year.

Things get even more interesting below, though. Xiaomi (4.2%, down from 5.7% in February) and AITO (3.9%, down from 5.4% in February) crashed and are not even keeping top 5 positions. So, we have two new players in the table — Tesla (5.9%, up from 5.4% in February), profiting from its peak month to surge into the 3rd position (a three-position jump), and Li Auto, joining the table in the 5th position with 5% share.

In the middle of all these changes, Wuling (5.2%) also profited from the chaos below the podium, climbing one spot and finishing March in 4th.

Below the top 5, the highlight is NIO (4.4%, up 1%), now in 6th place. Will the luxury maker be able to join the table in the coming months?

Looking at OEMs/automotive groups/alliances, BYD is leading, with 19.8% share of the market. It’s up 2.6% compared to the previous month. Meanwhile, #2 Geely lost 2% share and got down to 13.9%, seeing BYD put more distance between it in the race for #1.

Far from runner-up Geely, #3 SAIC (9%, down 0.4 percentage points) has lost share, as most of its brands continued on the slow lane.

Lucky for them that the most direct competition is still far away. Rising Changan (6.7%, up 1.2%) went up to 4th in March, but it is still over two percentage points below. Still, considering current trends, it wouldn’t be surprising if Changan could reach the podium by June.

Finally, Tesla returned to the top 5 OEMs, in 5th, with 5.9% share. Which was also last year’s final standing for Tesla in China and the Texan’s target for this year.

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News! Advertisement Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here. Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent. CleanTechnica uses affiliate links. See our policy here.CleanTechnica's Comment Policy